Goldman Picks Winners And Losers In Battle For $20 Billion COVID Antiviral Market

Goldman Picks Winners And Losers In Battle For $20 Billion COVID Antiviral Market

Ten days have passed since Merck dropped its bombshell announcement about Molnupiravir, its “revolutionary” anti-viral that purports to lessen severe COVID and death by half in vulnerable unvaccinated patients.

But as scientists warn about potential unexamined safety issues with molnupirvavir, analysts at Goldman Sachs are reminding clients that Merck is hardly alone in the race to produce an effective antiviral that could function like the Tamiflu of COVID.

Looking ahead to Q42021 and on to Q12022, Goldman is looking forward to drug readouts from Roche, Pfizer, Shionogi and others developing oral antivirals. Goldman’s discussions with clients about the potential influence of antiviralls “…indicate that key questions about oral antivirals largely center on: 1) clinical differentiation among the various programs; 2) data and approval timelines, supply, and pricing; and 3) the potential for pediatric and prophylactic use. Within, we size up the market potential and TAM with our market model and frame key upcoming readouts for the late stage programs. We also provide a list of upcoming catalysts in the category.”

For investors seeking “exposure to the antiviral theme”, Goldman recommends 1) Roche, as preclinical data for its AT-5227 suggest “differentiation” vs. molnupiravir, 2) Shionogi, whose S-217622 represents an alternative to RNA polymerase therapies, and 3) Divi’s Labs, which will ride molnupiravir’s coattails.

As for the losers, Goldman sees Eli Lilly and Regeneron, who produced antibody treatments that never really caught on.

Using the 10MM molnupiravir courses expected to be on the market for $700/course (40x what it costs to produce), Goldman estimates that the “commercial opportunity” for COVID antivirals is between “$15 billion and $20 billion.” That figure represents near-term sales; over time, Goldman estimates the market for COVID antivirals to be around $5 billion/$6 billion. Although the analysts look for prices to decline as more competitors are approved and enter the market.

Although Goldman’s team focuses on the “commercial” aspects of antivirals, its analysts note that their success could lead to significant “cultural” changes. If people were confident that COVID could easily be treated without a trip to the hospital, they would be less incentivized to wear masks and observe social distancing and other new features of the COVID era.

Goldman’s analysts put together a table showing their expectations for the timing of each drug’s approval.

{kind=link}

Goldman’s assessment about the TAM for COVID antivirals is based on the following assumptions:

COVID-19 becomes endemic in perpetuity, thereby requiring the maintenance of a vaccinated population as well as the use of effective therapies to treat those who are unvaccinated, immunocompromised, and breakthrough cases.

That following a relative peak of infections in the acute phase of the pandemic (starting late 2019 and still continuing) that the rate of infections will settle at a relatively consistent endemic level.

A relatively consistent vaccination rate in perpetuity that assumes maintained protection, boosters, and/or updated vaccines that experience the same relative uptake.

A lower rate of high-risk patients in the EU and ROW vs. the US. Generally, average BMI and hypertension rates are lower in the EU and Asia.

An average of 2 potential post-exposure prophylactic patients per infection, and that all major oral antiviral candidates will be approved in this indication.

That the post-exposure prophylactic population will be given an extended course of treatment compared to the primary treatment population as observed on both the Tamiflu and Relenza labels (e.g., 10 days vs. 5 days).

That the oral antivirals will significantly erode the antibody therapeutic market in the near term, particularly in the post-exposure prophylaxis setting due to their relative convenience and cost savings.

An initial price of ~$700/course in the US based on the previously announced government tender offer for 1.2mn courses of molnupiravir, and that prices will be relatively lower in the EU ($500) and ROW ($150).

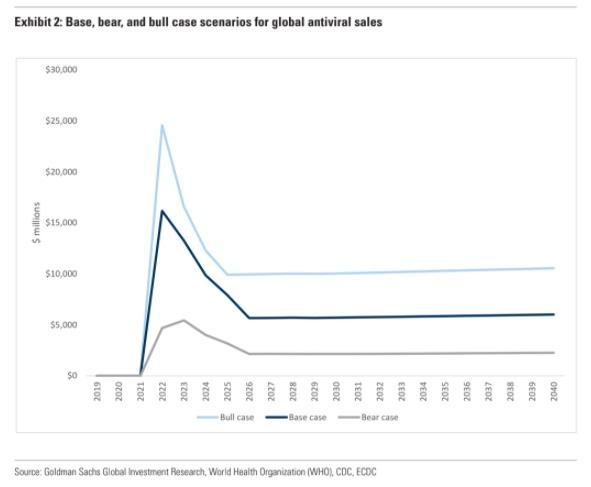

As far as sales, Goldman outlines its bull, bear and base cases in a chart.

{kind=link}

As far as what we know about molnupiravir so far is from a Phase 2/3 analysis with unvaccinated high risk patients.

{kind=link}

Looking at opportunities for distribution abroad, Goldman notes that Divi’s Labs should benefit from molnupiravir due to its ability to manufacture generic anti-retroviral API and finished doses. Citing data from – of all places – the Clinton health access initiative – Goldman says the overall market size in Low and Middle Income Countries is roughly $1.7 billion.

{kind=link}

Bottom line: in the coming weeks, the outlook for COVID anti-virals will become increasingly important to the market.

* * *

Source: Goldman Sachs

Tyler Durden

Wed, 10/13/2021 – 17:05

Originally appeared on Read More

BREAKING NEWS

- Florida man shoots family dog in the face during argument over infidelity: police

- Anti-Israel agitators continue disruptions with escalations at USC, Harvard and Columbia

- How US workers could be affected by changes to ‘noncompete’ agreements and overtime pay

- Bottlenose dolphin found shot to death in southwest Louisiana

- Chinese student gets 9 months for harassing person posting democracy leaflets on Boston campus

- ATF Rule-Change Creates A Trap For The Unwary

- Biden’s $60BN Can’t Fix Ukraine’s Manpower & Recruitment Crisis

- COVID-19 Vaccine Protection Among Children Plummets Within Months: CDC Study

- Israeli Strikes More than 40 Hezbollah Sites, Defense Minister Claims South Lebanon Command is Decimated After Half of Hezbollah’s Commanders Killed

- With His Wife Indicted for Corruption, Spanish Socialist PM Sánchez Is Considering Resigning

Leave a Reply