“Biggest Dovish Shock” From Australia Since 2008 “Supercharges” Bets That Global Tightening Is Ending

“Biggest Dovish Shock” From Australia Since 2008 “Supercharges” Bets That Global Tightening Is Ending

One month ago we said that there is a reason why despite fundamentals, yields and newsflow screaming for lower prices, US equities simply refused to sell off: it was because investors know that the moment the Fed pivots dovish and capitulates on its tightening cycle (a move which could take place at any moment since it is as much political as it is financial), risk will explode limit up. And so, even though the US is sliding into a recession – or rather because the US is sliding into a recession – stocks remain sticky to the upside, and the VIX barely rises to crisis levels, waiting for the inevitable pivot.

Also one month ago, we got an advance look of what said pivot would look like courtesy of Australia, where bond yields tumbled and stocks soared after the country’s top central banker opened the door on Thursday to slowing the bank’s policy tightening after five rate increases in as many months, sparking a rally in bonds as markets scaled back bets on further aggressive moves.

In a speech on the policy outlook, Reserve Bank of Australia Governor Philip Lowe said further rate increases would be needed to contain inflation but the RBA Board was not on a pre-set path and was aware rates had already risen sharply: “We are conscious that there are lags in the operation of monetary policy and that interest rates have increased very quickly,” said Lowe adding that he recognizes that “all else equal, the case for a slower pace of increase in interest rates becomes stronger as the level of the cash rate rises.”

{kind=link}

Investors quickly read between the lines and sent Australian bonds yields tumbling.

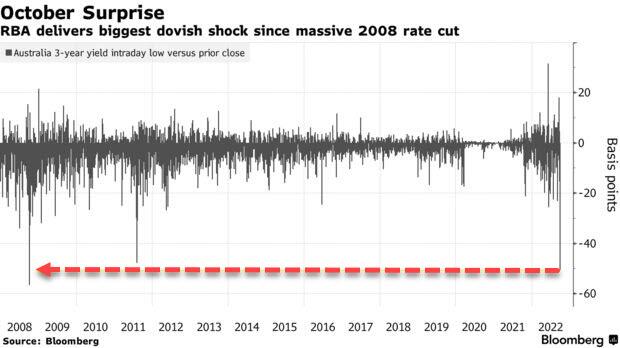

But it was nothing compared to what happened this morning, when yields on rate-sensitive three-year Australian government bonds plunged by the most since 2008 after the central bank raised interest-rates by a less-than-expected 25 basis points, in what Bloomberg said was “the biggest dovish shock since 2008.”

{kind=link}

Adding to today’s surprise is that the RBA ended a streak of outsized increases, a result predicted by only a quarter of economists surveyed. And as we noted earlier, the shockwave from the unexpected move – not quite a pivot yet, but this close – quickly spread around the world, giving a fresh boost to the rally in Treasuries, pushing New Zealand yields lower and helping turbocharge a rally in Japanese equities.

As Bloomberg also said, the Reserve Bank of Australia’s dovish surprise would be interpreted by some as a “supercharged” sign that the end is in sight to the wave of aggressive monetary tightening that has steamrolled global bonds and equities this year. Australia – whose economy is extremely reliant on a housing market which has gotten slammed due to soaring mortgage rates – has acted as a lead indicator for at least the bond market since late 2021, when the RBA’s sudden abandonment of curve control sent local yields spiking.

Still, any global read-across is complicated by the fact that Australian policymakers are mindful of the indebtedness of their household sector and the prevalence of variable mortgage rates which means hikes are particularly impactful.

“I think we are getting to the point where markets are pricing in peak rates,” said Ned Bell, chief investment officer at Bell Asset Management, a global equities fund manager based in Melbourne. “You will start to see the trajectory of inflation moderate and that should be a good sign that you’ll see similar moves from what we’ve seen from the RBA today. The magnitude of rate hikes will slow.”

The RBA shock came one day after the US manufacturing ISM index gave the latest indication the US economy is faltering and before today’s dismal JOLTS reports confirmed the recession is finally spreading to the labor market.

Meanwhile, as Bloomberg notes, a growing cohort of investors are also scooping up bonds, with the likes of Citigroup’s Steven Wieting and JPMorgan drawn by attractive valuations and growing bets for an economic downturn. Two-year Treasury yields fell about eight basis points to 4.08% on Tuesday, adding to the 17 basis point decline on the prior day; it briefly dropped below 4% despite expectations for aggressive Fed hikes at least into Q1 2023. The three-year Australian bond yield plunged 32 basis points, while the nation’s benchmark stock index rallied by the most since June 2020.

“Central banks are grappling with inflation and other growth/leverage factors,” said Viraj Patel, strategist at Vanda Research. “More central banks will be taking it slow in Q4.”

“The RBA is clearly dancing to its own tune,” said Andrew Ticehurst, a rates strategist at Nomura Holdings. “The other major G-10 central banks have been delivering a consistently more hawkish message in our view.”

And with Australia set to capitulation in its fight against inflation, all eyes now turn to the Reserve Bank of New Zealand, which is set to announce its monetary policy decision on Wednesday with some economists expecting a signal of continued tightening.

The New Zealand central bank is expected to raise interest rates by 50 basis points for a fifth straight time, according to economists surveyed by Bloomberg. A hawkish surprise from the central bank at the forefront of global rate hikes could knock the wind out of bond bulls’ sails; of course a dovish surprise would confirm that the pivot is now imminent.

“The RBA decision will stoke speculation that other central banks will begin slowing the pace of hikes,” Prashant Newnaha, strategist at TD Securities, wrote in a note. “We’ll see if RBNZ walks the same path tomorrow.”

Strategists like Australia and New Zealand Banking Group Ltd.’s John Bromhead cautions against betting on rates peaking globally too quickly particularly from the Federal Reserve, despite Tuesday’s dovish surprise.

“Rhetoric from virtually all the Fed members so far is they are cautious of making a 70’s style mistake — by pausing too early,” he said. “I’d be cautious of extrapolating RBA decisions too far.”

Tyler Durden

Tue, 10/04/2022 – 11:20

ZeroHedge NewsRead More

BREAKING NEWS

- Oklahoma man ‘bludgeoned’ girlfriend’s relative with brick before dumping remains in wildlife refuge

- You Are Not the President of Anything

- Student Protester at NYU Appears Unaware Why She is Even There – Turns to Question Friend (VIDEO)

- Armed Secret Service Agent Assigned to Kamala Harris Gets Into Fight with Other Agents at Joint Base Andrews, Has to be Physically Restrained

- Left Wing Daily Show Mocks Joe Biden Over Cannibals Comments: ‘You’re Going to Lose the Election’ (VIDEO)

- Riley Gaines, West Virginia AG Take Transgender Sports Ban Fight to Supreme Court

- Another State Passes Legislation to Give Hope, Treatment to the Terminally Ill

- EXCLUSIVE: LA County Assistant DA Over Ethics and Integrity Stole Thousands of LA Sheriff Personnel Files

- Florida man shoots family dog in the face during argument over infidelity: police

- Anti-Israel agitators continue disruptions with escalations at USC, Harvard and Columbia

Leave a Reply