IMF Issues Global Stagflation Alert: Cuts Global GDP As It Warns Of Rising Inflation And “Dangerous Divergence”

IMF Issues Global Stagflation Alert: Cuts Global GDP As It Warns Of Rising Inflation And “Dangerous Divergence”

In its latest World Economic Outlook report published on Tuesday morning, the International Monetary Fund voiced its starkest caution about stagflation yet, warning that the global economic recovery has lost momentum and become increasingly divided, even as it warned about rising inflation risks.

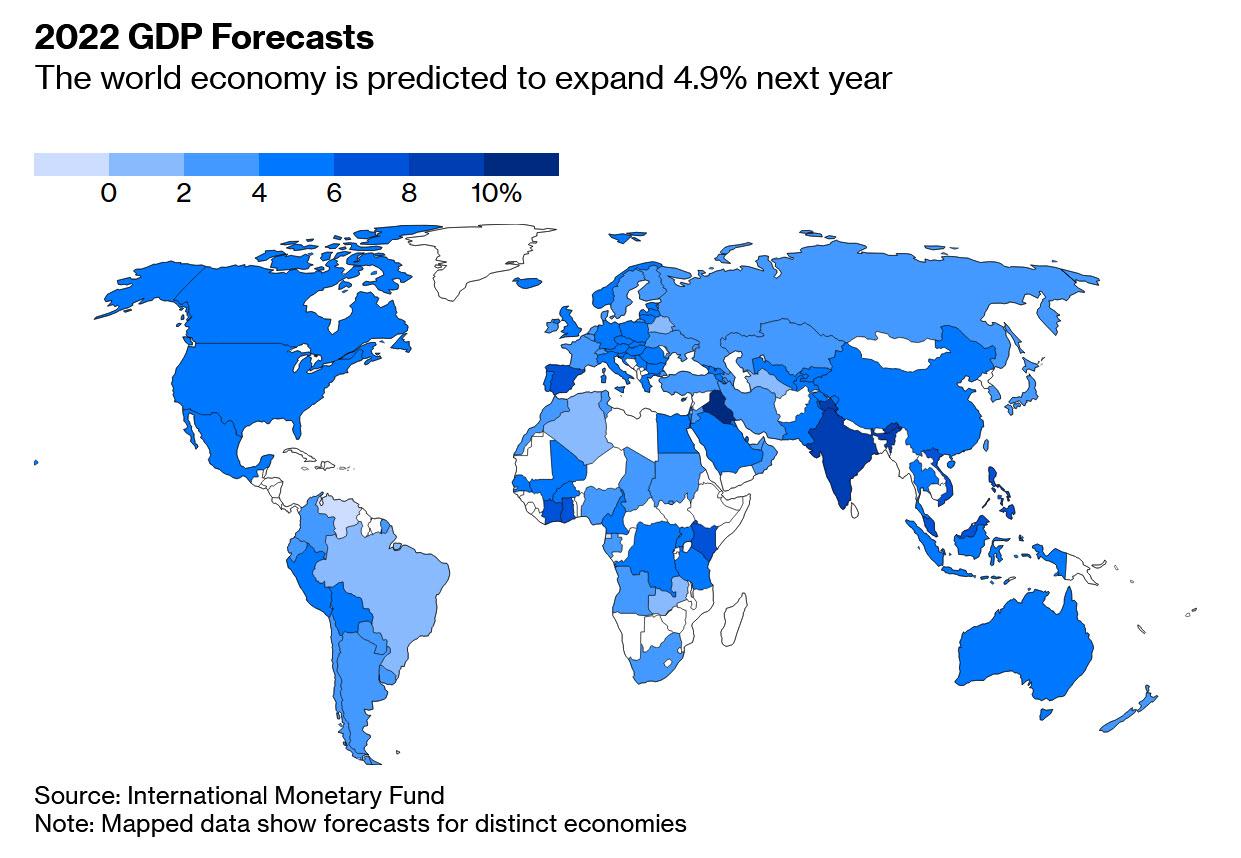

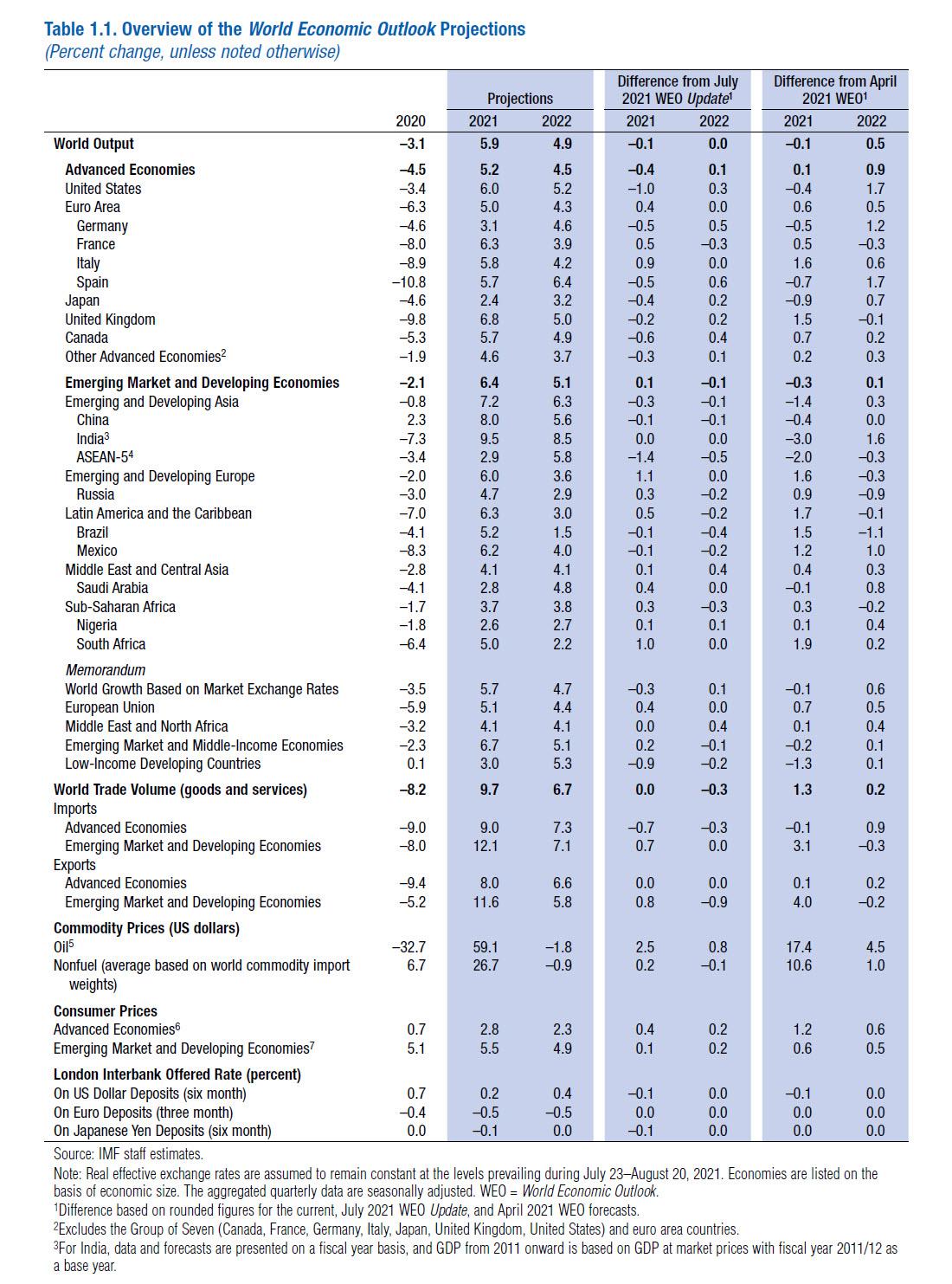

The fund warned threats to growth had increased, pointing to the delta variant, strained supply chains, accelerating inflation and rising costs for food and fuel. As a result, the IMF trimmed its global growth forecast and now expects world GDP to rise 5.9% this year, down 0.1% from what it anticipated in July and a bounce from the 3.1% contraction of 2020. The 2022 forecast was unchanged at 4.9%.

{kind=link}

The IMF also cautioned that this modest headline revision “masks large downgrades for some countries” adding that “the outlook for the low-income developing country group has darkened considerably due to worsening pandemic dynamics. The downgrade also reflects more difficult near-term prospects for the advanced economy group, in part due to supply disruptions. Partially offsetting these changes, projections for some commodity exporters have been upgraded on the back of rising commodity prices. Pandemic-related disruptions to contact-intensive sectors have caused the labor market recovery to significantly lag the output recovery in most countries.”

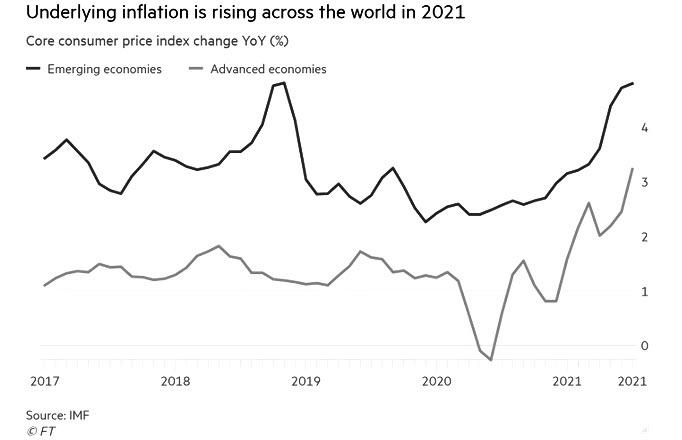

Pointing to this “dangerous divergence” in economic prospects across countries, the IMF said that this remains “a major concern.” And while the IMF trimmed its growth outlook, it also warned that the global economy is entering a phase of inflationary risk, and called on central banks to be “very, very vigilant” and take early action to tighten monetary policy should price pressures prove persistent.

{kind=link}

“Emerging and developing economies, faced with tighter financing conditions and a greater risk of de-anchoring inflation expectations, are withdrawing policy support more quickly despite larger shortfalls in output” the report cautioned.

“Overall, risks to economic prospects have increased, and policy trade-offs have become more complex,” Gita Gopinath, the fund’s director of economic research, said in the report’s introduction. “The dangerous divergence in economic prospects across countries remains a major concern.”

Among the world’s biggest economies, the IMF cut its 2021 forecast for the U.S. by a full percentage point to 6%, mainly because of supply constraints, but boosted its 2022 estimate to 5.2% from 4.9%.

The IMF also forecast that China will grow at a rate of 8% this year and drop to 5.6% next, both a decline of 0.1 point from July; expect both of these to be revised sharply lower as Citi warned that China is now entering a period of acute, if brief, stagflation. Countering this, the IMF raised its projection for the euro area to 5% for this year from 4.6%, and kept its 2022 estimate at 4.3%. Forecasts for Japan, the U.K., Germany and Canada were all cut for this year, but lifted for 2022. Low-income countries were tipped to advance just 3% this year, a slicing of 0.9 point from July.

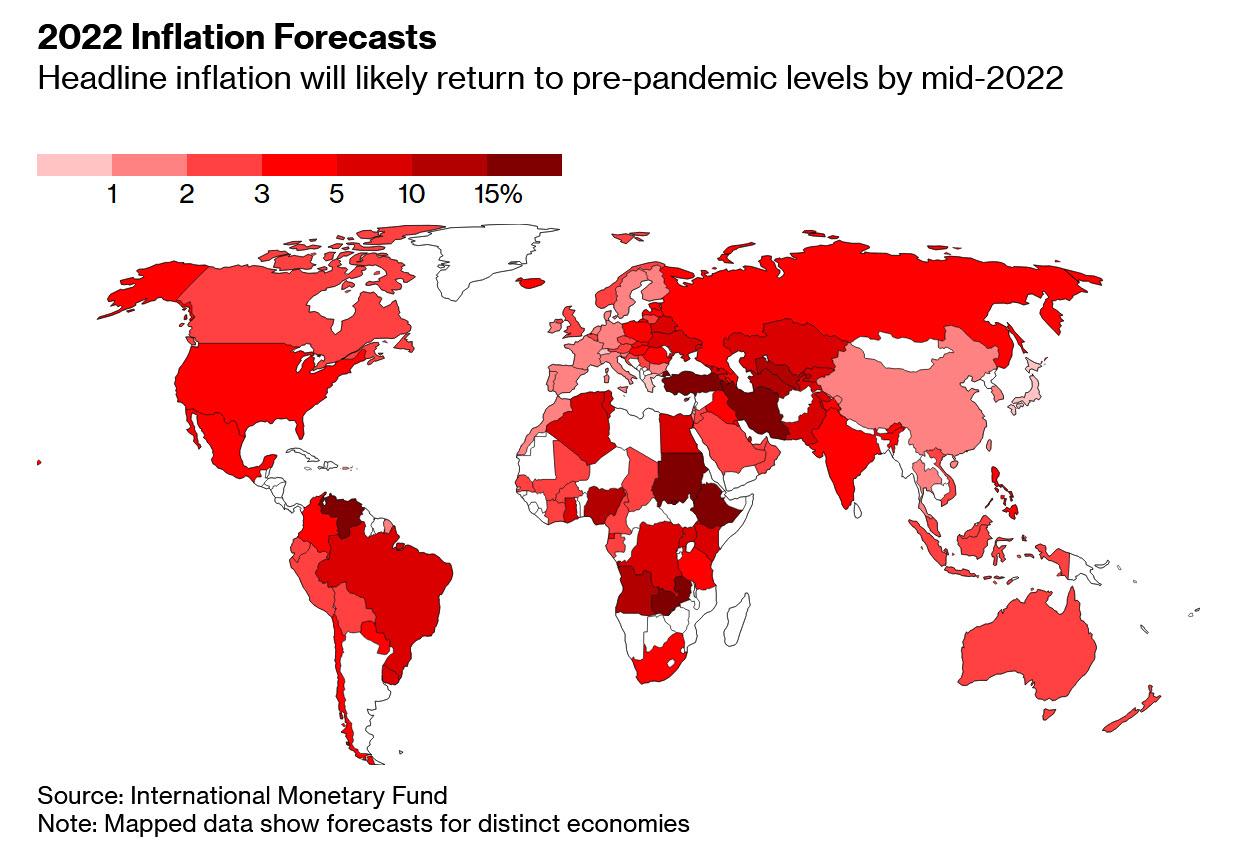

Still, it wasn’t all bad: as investors are growing increasingly concerned about the threat of stagflation, the IMF provided some comfort by saying inflation will subside to 2% in advanced economies by the middle of 2022 after peaking in the final months of this year, in other words it took is in the “transitory” camp. But it bet emerging and developing economies would still see consumer prices gain 4.9% next year after 5.5% this year.

{kind=link}

The IMF calculated gross domestic product for advanced economies will regain its pre-pandemic level in 2022 and even exceed it by 0.9% in 2024. But only two-thirds were seen regaining their earlier employment levels. In contrast, it predicted that emerging and developing markets would still undershoot their pre-pandemic forecast by 5.5% in 2024.

The disparity is based chiefly in differences on vaccine access and policy support. About 60% of people are vaccinated against Covid-19 in rich countries, but less than 5% in low-income nations, it said. Emerging economies are also withdrawing policy support more quickly and face outsized pain from costlier food.

Overall, the fund cautioned that inflation risks are “skewed to the upside” and those for growth are “tilted to the downside.” Sounds like a pretty clear warning that stagflation is imminent to us, even if Gita Gopinath, the IMF’s chief economist, said the strength of the economic recovery meant it was too early to “say anything about stagflation”, despite some supply shortages which have also boosted inflation.

“We always knew coming out of this deep contraction that the supply-demand mismatch would pose problems,” she told the Financial Times. “The hope was that it would even itself out by around this time of the year . . . But we’ve been hit with additional shocks, including some weather-related shocks, that certainly makes that imbalance persist longer,” Gopinath said.

The IMF’s central forecast is that inflation will rise sharply towards the end of the year, moderate in mid-2022 and then fall back to pre-pandemic levels, similar to the prevailing central bank narrative. But its report also noted that “inflation risks are skewed to the upside” and advised central banks to act if price pressures showed signs of lasting.

{kind=link}

Hilariously, even as it warned about rising inflation threats, the fund said central banks should generally ignore higher prices that stemmed from energy price shocks or temporary difficulties in bringing products to market. But it should act if there are signs that companies, households or workers start to expect high inflation to linger.

“What [central banks] have to watch out for is the second-round effects [with] these increases in energy prices feeding into wages and then feeding into core prices. That’s where you have to be very, very vigilant,” Gopinath said.

The report was clear that “central banks . . . should be prepared to act quickly if the recovery strengthens faster than expected or risks of rising inflation expectations become tangible”.

That means getting ahead of the curve on prices even if employment is still weak, the IMF recommended, as that is preferable to allowing inflationary mindsets to become ingrained. “A spiral of doubt could hold back private investment and lead to precisely the slower employment recovery central banks seek to avoid when holding off on policy tightening,” the IMF warned.

In other words, don’t do anything if inflation is transitory but step in quickly if it isn’t. If only central banks knew which is which.

There was another warning: the IMF said that In financial markets “stretched asset valuations” meant investor sentiment could shift rapidly by adverse news on the pandemic or policy. Amid pressing concerns are the impasse over the U.S. federal debt limit and possible weakness in China’s property sector.

Finally, the IMF also had some suggestions on the biggest strawman issue around: climate change. As a meeting of international governments on fighting climate change nears at the end of the month, the fund said “stronger concrete commitments” are needed, including tailored international carbon price floors and $100 billion of support for developing nations. It also called again on rich countries to channel a recent bolstering of IMF resources to more needy counterparts.

Looking further out, the fund said if Covid-19 has a prolonged impact, it could reduce global GDP by $5.3 trillion over the next five years relative to current projections. That could be offset if governments intensify efforts to equalize vaccine access.

Tyler Durden

Tue, 10/12/2021 – 09:35

Originally appeared on Read More

BREAKING NEWS

- Anti-Israel protesters at Florida universities can be ‘expelled’: DeSantis

- Alabama sets execution date for man convicted of killing delivery driver during attempted robbery

- Russia Will Target US Nuclear Weapons In Poland If They Appear

- EU Prepares To Tighten Screws On Russian LNG Imports

- Boeing Flight Carrying 345 People Bounces on LAX Runway During ‘Rough Landing’

- Planes Almost Collide at 2 Major Airports as Boeing Probe Advances

- Los Angeles suspect who ‘targeted’ mayor’s house had troubled past, dad says

- Texas homeowners who finally evicted squatter ‘treated like criminals’

- Americans face ‘direct’ threats from foreign dictators, terrorists, migrants: 3 things to know

- European ESG Funds Witness Heavy Decline In Inflows

Leave a Reply